For decades, Americans viewed life insurance as a “set it and forget it” task—a line item on a checklist completed once and buried in a filing cabinet. But as we move through 2026, a “perfect storm” of economic volatility, rising living costs, and technological shifts has created what experts call a “Dangerous Coverage Gap.” Today, a policy that seemed “adequate” just five years ago might now leave a family struggling to maintain their standard of living. Here is a deep dive into the three major shifts redefining family protection this year.

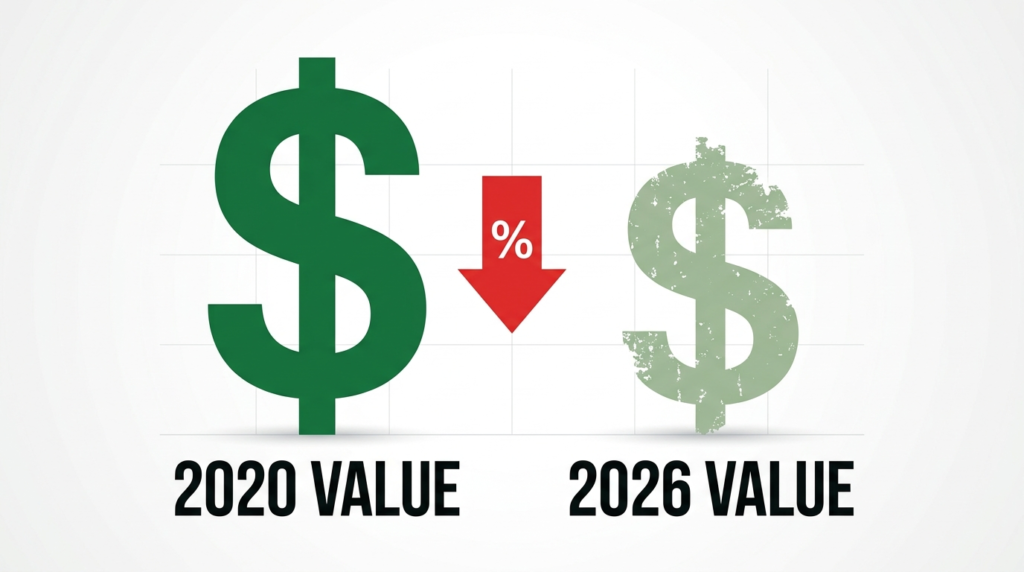

1. The Inflation Trap: Why $500,000 is the New $350,000

The most invisible threat to family security is the cumulative effect of inflation. While your policy’s face value remains the same, the real-world purchasing power of that payout has eroded significantly.

“Many families calculate their needs based on yesterday’s prices,” says one senior financial analyst. “But with the rising costs of mortgages, healthcare, and university tuition, that legacy payout may now fall short by 30% or more.”

The solution for many has been the **”Smart Switch.”** Instead of simply adding more cost to an old, expensive plan, savvy consumers are now using State-of-the-art rate comparison platforms to shop the entire 2026 market. By doing so, many discover they can double their death benefit while paying the same—or even less—than their outdated premiums. It’s no longer about buying more insurance; it’s about buying smarter insurance.

2. The Rise of “Financial-First” Pricing Models

One of the most significant shifts in 2026 is how insurance companies determine who gets the best rates. We are seeing the end of the “one-size-fits-all” premium.

In the past, your health was the only major factor. Today, sophisticated algorithms prioritize your “Financial Health Profile.” Actuarial data shows a direct correlation between responsible financial habits and long-term stability. As a result, those who maintain solid standing are being rewarded with the most competitive rates available — benefits that were previously out of reach.

Because of this, experts now recommend a strategic two-step process. Before applying for a new policy, smart applicants are first checking their credit profile to ensure their financial standing is accurately reflected — a step that can directly impact the tier of rates they qualify for. By verifying this data beforehand, you position yourself to qualify for the lowest possible tier, potentially saving thousands of dollars over the life of the policy.

🟢 Special Segment: Why Life Insurance is the Ultimate 2026 Asset

In a volatile economy, life insurance has evolved from a simple safety net into a critical pillar of wealth protection. It is the only financial instrument that guarantees immediate, tax-free liquidity for your family at the exact moment they need it most.

Unlike a savings account or a 401(k), which can be subject to market crashes or lengthy probate periods, a modern life insurance payout bypasses the red tape. It ensures that mortgage payments are met, education continues, and the family’s legacy remains intact. Leaving your family’s future to “savings alone” is a gamble that most experts no longer recommend.

3. The Death of the Waiting Period: The Digital Revolution

Perhaps the most welcome shift for consumers in 2026 is the collapse of what industry insiders call the “Bureaucratic Nightmare.” For years, the single greatest barrier to obtaining life insurance coverage was the mandatory medical exam — a process that could stretch across weeks, requiring home visits from paramedical nurses, multiple blood draws, and lengthy underwriting reviews.

According to a 2025 report by the Insurance Information Institute, the average time-to-coverage for a traditional term life policy was 4 to 6 weeks. For many families, that window of vulnerability was simply unacceptable.

That is now changing rapidly. A new generation of **fully digital, instant-decision platforms** has emerged, replacing invasive procedures with real-time data science and algorithmic underwriting. Industry data suggests that qualified applicants on these platforms are now receiving coverage decisions in under five minutes — a 98% reduction in processing time compared to the traditional model.

“We are witnessing a fundamental restructuring of how Americans access protection,” notes one senior actuary at a leading risk analysis firm. “The technology has matured to the point where physical exams are simply no longer necessary for a significant portion of applicants.”

For consumers, the implications extend beyond speed. These next-generation platforms also offer dynamic coverage adjustments, allowing policyholders to scale their protection up or down as their financial circumstances evolve — all managed entirely online.

The Bottom Line

The 2026 market belongs to the informed consumer. Whether you are looking to lower your current monthly costs, close a coverage gap caused by inflation, or simply secure your first policy without the hassle of a medical exam, the tools are now at your fingertips. The message from experts is clear: Don’t wait for a health scare or a market correction to check your eligibility for 2026’s top-rated plans.

✅ Verify your financial health status to qualify for the most competitive rates available.

✅ Use a comparison tool to identify coverage gaps in your current policy.

✅ Apply through an instant-decision platform to skip the 6-week medical exam wait.